Workplace Pension Registration

The impact of auto-enrolment on workplace pensions has been immense. Many thousands of workers are now more secure in retirement because all UK companies are required to offer a pension to employees.

Employers also benefit from a more confident and stable workforce. It’s not always easy for them. Getting registered with pension regulators and compliance with government regulations is a challenge for small businesses.

Get workplace pension registration done by the expert!

Crawley’s Best Tax Accountants For The Payroll

Services

How Workplace Pension Accountant Can Help

Workplace Pension Accountant or Auto-enrolment Accountant provides various services related to a workplace pension.

We help clients to find the right information and advice in order to help them choose the right pension scheme and setup pension scheme; and make sure they comply with workplace pension regulations. Understanding the details of workplace pensions for those who own a business or employ a spouse/partner.

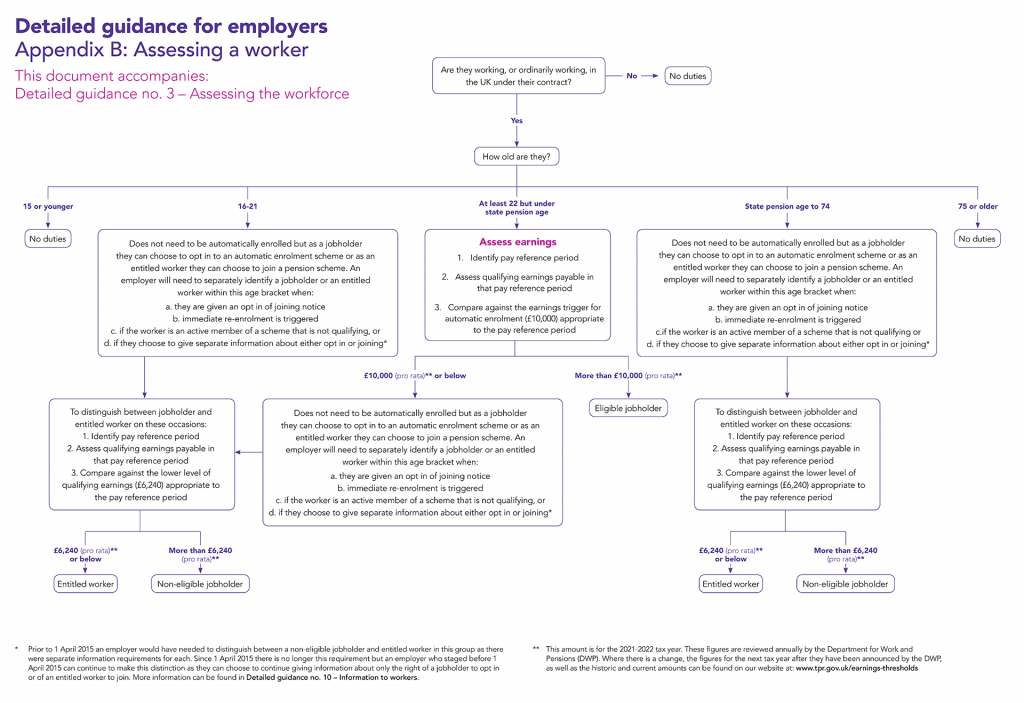

- Eligibility Criteria:

All staff members who:

- are aged between 22 to state pension age

- have income of more than GBP 10,000

- are working in UK

Staff who do not meet these criteria may opt in for auto-enrolment. You must enrol them if they opt in.

A company that has a single director and no employees, will not be classified an employer for auto-enrolment purposes. However, you must notify The Pensions Regulator that your company is not an employer. If more than one director is being paid, they can choose to not be enrolled. However, they will need to submit a declaration to compliance.

.

We can help you in evaluating the pension costs and the effect of pension cost on financials of the entity.

We can assist you in communicating with employees about auto-enrolment, benefits of pension scheme; and explaining various aspects related to pension.

We can help you in setting up pension scheme for self-employed, a company pension scheme for directors, and pension scheme for small company.

Automatic Enrolment

As per the Pension Act 2008, Every employer in the UK is required to enrol certain employees into a workplace pension scheme and make a contribution. This is known as ‘automatic enrolment‘. Employer has certain legal obligations.

Register with The Pension Regulator

To confirm that an automatic enrolment program is in place, employers must register with The Pensions Regulator within five months of their staging date. Non-compliance may lead to enforcement actions.

Communication with employees regarding auto-enrolment

All the affected staff should be notified about auto-enrolment in written.

After they are automatically enrolled, staff can opt out of the pension scheme. If someone wish to withdraw, he has to complete the form provided by pension provider and submit it to the employer.

FAQ

Most frequent questions and answers

Such employee will not be auto enrolled however they may be categorized in either ‘entitled worker’ or ‘non-eligible worker’. The entitled job holder may opt-in for pension scheme voluntarily. Auto-enrolment criteria only determine who shall be auto-enrolled. Other staff may enrol to pension scheme by their choice.

Yes, the employer as well as the employee can contribute more than the minimum requirement if allowed by pension scheme provider.

As per law, contributions must be paid by 22nd day (19th day in case paid by cheque) of the next month. Also, date of payment must be agreed with pension scheme provider.

On late payment, fine may be imposed by The Pension Regulator.

This selection has to be made among various pension schemes including defined contribution, defined contribution and hybrid schemes.

In case of defined contribution workplace pension scheme, Employer has to check with Pension Regulator whether it can be used for auto-enrolment.

In case of stakeholder pension scheme, it needs to be operated till existing members want. Employer don’t have the obligation to offer it to your employees.

Depending on the pension scheme you choose, the amount that you and your employees contribute may differ. Your staff and you must contribute a minimum amount to your pension scheme by law. The total contribution is set to minimum 8% of employee’s earning. Employer’s minimum contribution is 3% however he may choose to contribute more.